At Affinity, we believe that a strong, unified culture and symbiotic relationships are the keys to our success. ...

As we close out another not-so-normal year, it’s time to reflect on what we’ve learned. We asked a few Affinity team ...

Excel can do so many things that just getting started can be intimidating. While you can transform your data with ...

Finding Windows settings has never been easier. The days of needing to navigate through the Control Panel to change ...

Everyone sends emails. Some of us send a lot of them. And, why not? It’s convenient, accessible everywhere (for good ...

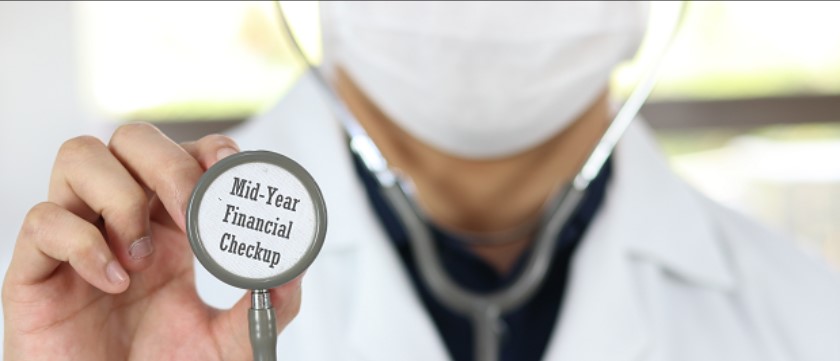

Year-End…a word that triggers stress in some and at mid-year, procrastination in others.

Are you tired of fishing ugly HDMI and VGA cables around your conference room to do a presentation or conduct training?

Moneyball Analytics is based on the book Moneyball, The Art of Winning an Unfair Game by Michael Lewis. The book became ...

Legal writing is full of symbols. Inserting symbols using the Ribbon can take several mouse clicks. There is a faster ...